Byrne Hobart

Byrne Hobart

Match Group and Managed Dissatisfaction

Online dating is many things:

- It's a classic easy-to-start but hard-to-fund business, leading many companies to try it and many of those to pivot away: YouTube was originally a dating site, and while Facebook wasn't strictly a dating site at first, it certainly used to emphasize relationship status more (and this is fractally true: Facebook's former Head of International Growth a decade ago had previously started a dating site for Harvard students that required an @harvard.edu email address).

- An industry that can support some good-sized companies, like Match (market cap: $32bn) and Bumble (market cap: $5bn).

- Despite the fact that it looks like a trivial business, it's arguably the world's most important software industry, and one that governments should care deeply about. As it turns out, CFIUS demonstrated some foresight when they unwound a Chinese company's acquisition of Grindr.

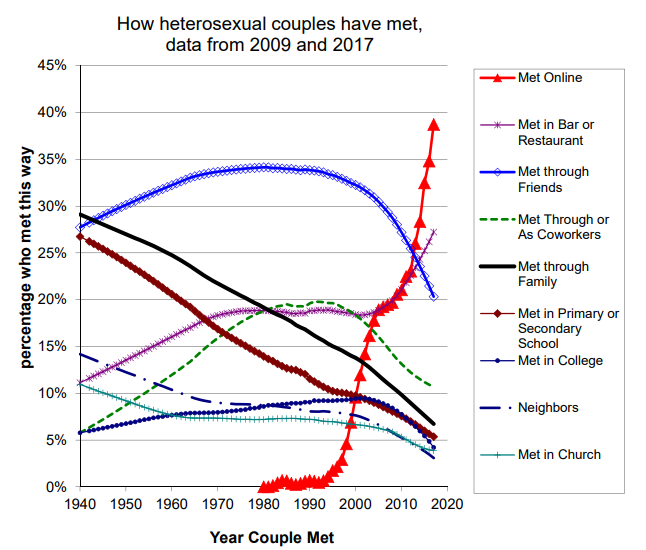

The impact of online dating on relationships is staggering:

Online dating is displacing every other form of matchmaking, and this graph actually understates it—an important thing people in the online dating business learn is that online daters are pathologically dishonest, but generally incrementally so; as it turns out, a surprising number of heights round up to exactly six feet, and an astonishing range of dealbreakers don't actually break deals. So when you look at a chart indicating that "Met in a Bar or Restaurant" took off as a how-we-met story right alongside the ubiquity of cheap broadband and the smartphone, you can comfortably attribute those gains to online dating, too, from people who are slightly embarrassed to admit it.

If online dating determines how most people meet, that means it's a marginal determinant of who has kids, with whom, and when. And that's a pretty big deal: if online dating encourages longer courtships than people would otherwise prefer, for example, it delays family formation, and that warps the demographic pyramid and slows economic growth.1

Over time, dating apps have approached a stripped down, mostly image-focused, volume-driven, swipe-based interface. This describes Tinder (the prize asset of Match) and Bumble. One interesting feature of these apps is that they're marketplaces, where both sides need an incentive to join and where the central marketplace can tweak their individual incentives in order to either a) get more users who attract other users, or b) get more users to pay. One of the gaps between Tinder and Bumble is that Bumble restricts the first message to female users once a match is made, while on Tinder either side can message first. This maps nicely to how exchanges provide rebates to price makers and charge fees to price-takers: if there's one side of the market that's harder to get than the other, that side gets paid.2

There's a common pattern where any social site grows because it's cool and then stops being cool because it's grown. Exclusivity and uniqueness is a great marketing hook, but ubiquity pays better. This applies across many domains: LinkedIn-without-the-recruiter-spam is LinkedIn-but-too-small-and-undermonetized-to-compete-with-the-real-LinkedIn. One of the drivers of this is the fact that Tinder-style economics are much better; look at how the feed on Facebook or the timeline on Twitter have changed over the years and it's clear that images retain users better than words. But it's also driven by Match Group, which has been a serial acquirer of smaller dating sites.

Match has an interesting backstory: it was founded in 1993, originally as a general online classifieds site (the founder bought other brand names like Jobs.com and others). The company was sold for $7m in 1997 in a deal that netted its founder just $50,000, and then sold again to Ticketmaster Citysearch for seven times as much eighteen months later. Through that acquisition, it ended up at IAC.

IAC is a quirky holding company that has evolved into an incubator designed to grow and then spin off sub-companies. That model has some inefficiencies—the company doesn't centralize functions like accounting, so there are duplicated costs. On the other hand, it turns the parent company into a financially-optimal basket of options, which can easily break out reporting for promising segments and then spin them off at opportune times. IAC is confident enough in the company-incubating business that it lets its sub-companies compete against one another (in fact, Tinder was incubated by IAC, not by Match, before the two were joined under the same parent company).

Part of IAC's dealmaking lineage stems from the career of their chairman, Barry Diller. Diller is one of those exceptionally ambitious and unusually durable individuals who managed to be notable both for what he accomplished when he was young and for the fact that he kept working when he was very old (Donald Rumsfeld, who holds the record as youngest-ever Secretary of Defense under Ford and oldest-ever under Bush, is another example). Diller came up in the TV business, which is very deal-centric; TV executives are constantly making show acquisitions that might or might not pay off, structuring contracts for maximum advantage, figuring out what to do with excess cash flow when times are good, or scrambling for cash when times are bad. It may not be a coincidence that this pace of dealmaking can only be replicated by having a wildly diversified holding company with a penchant for acquisitions and divestitures across many different business lines.

Success for the online dating business means controlling the cost of customer acquisition—easier with an intrinsically viral product, at least on the way up—and then minimizing churn. Which, for users, means that an experience that feels promising but ultimately keeps them in the dating world indefinitely is ideal for the company. Match Group has compounded its paying user count by 23.3% annualized over the last five years, and an astonishing 16.2m people use their services, 10.6m of whom are Tinder users. These users pay an average of $16.16 per month, a number that's been creeping up in recent quarters but that isn't quite comparable to their historical numbers.3 And that top-line growth has produced some healthy profits; Match's EBITDA margin was 12.8% in 2016, and 30.9% at the end of this year: businesses with network effects and many in-app payment levers to tweak can produce great incremental margins at scale.

The optimal state for the dating business recalls a term from Blockbuster's history: "managed dissatisfaction" meant that they expected not to have the most in-demand movies all the time—buying enough VHS tapes to meet demand for the first week of availability meant having far too many a few weeks later, and VHS tapes were pricey. So they aimed to get customers in the door with the prospect of new releases, and then gave them enough options to rent something acceptable instead. While Tinder doesn't necessarily deliberately target a system where people meet someone they'd see a few times but not settle down with, the tweaks that push the product in that direction are the ones that improve the churn numbers.

The trouble with the managed-dissatisfaction model is that it means that anyone who offers a better experience is an automatic winner, at least if they can afford to market it. And that's not an easy problem in the dating business, where pairing off users permanently means getting higher churn, which both cuts into revenue and makes the site less attractive to new users. There have been many alternatives to this attempted over time: HowAboutWe tried to mix online dating with group buying, so it could monetize a relationship rather than indefinite singledom (it didn't take off, and is now a subsidiary of Match Group); OKCupid used quizzes to match users with compatible personalities, but once it was swallowed by Match as well it turned into something more generic4; eHarmony has tried to match users for long-term relationships, and is apparently viable but small; various niche efforts in paid matchmaking have been tried recently, and it remains to be seen how they do. So the current online dating industry may be a very low local maximum: there are benefits to disrupting it, but the nature of social sites and the inescapable tyranny of customer lifetime value mean that the path to the next local maximum is treacherous indeed.

A Word From Our Sponsors

If you’re frustrated that your bank account isn’t crypto-friendly, it’s time to make a change. Meet OnJuno, a Sequoia-backed startup that helps you earn, save, and invest in crypto directly from your checking account.

With OnJuno, you can:

- Set up your direct deposit and get a portion of your paycheck in crypto!

- Buy crypto instantly with zero fees

- Yield 4% on your USDC without any lockups

There’s no catch. OnJuno integrates directly with your direct deposit system, has no transaction fees, and is already being used by employees at Apple, Google, Amazon, Microsoft, and Uber. It's free to open an account and today you can get $50 added to your first direct deposit when you use the code DIFF.

Elsewhere

Revolving Doors

The WSJ reports that Jared Kushner is raising money for an investment fund that will focus on the Middle East ($). It's a revolving-door deal in two respects: the fund plans to focus on opportunities that arose from better relations between Israel and other Middle Eastern countries, something Kushner played a role in when he worked at the White House. And some of the investors considering the fund apparently think it would be valuable to have a relationship with Kushner on the off chance that he'll be back in government soon. In one sense this sets up some nice opportunities: peaceful and stable diplomatic relationships create wealth for the world, among their many other positive benefits, but successful diplomats aren't exactly collecting a commission on this. The ambiguity makes it tricky: someone who works for the government and then moves into the private sector permanently is playing a one-shot game, while going back and forth between the two is an iterated game where there's an incentive to set up deals that are not necessarily helpful for everyone but are very lucrative for someone. (As in other areas, Singapore sets a good example by paying government officials salaries competitive with the private sector so there's less of an incentive to go back, or to go back and forth.)

Sanctions

Do US sanctions matter to a country that sells globally-useful natural resources, and who can sell them to entities that aren't directly affected by sanctions? Reuters reports that Russian oil companies are having difficulty getting letters of credit to sell oil: both sides of the oil transaction are apparently willing and able to do business, but the financial intermediaries aren't. The omnipresent dollar and an increasingly financialized global economy are a force multiplier for US sanctions: as soon as an activity interacts with the financial system, the US government gets a veto by threatening to cut participants off from a) dollars, and b) any cautious counterparties who use dollars. Deals may still happen; high prices make people more tolerant of otherwise crazy risks. But this does show that US rules can be disruptive in financial terms even if a country has enough real resources to get by.

(Meanwhile, in an effort to be less dependent on the dollar, Russia is taking a closer look at crypto. The wonderful thing about a distributed, permissionless system is that it's immune to rules. The annoying thing about it is that intermediaries who want to interact with the US financial system are not immune to rules, and will face something between inconvenience and existential risk if crypto becomes, or is perceived as, a way around sanctions. If you’re trying to follow the rules while building your company around a product that, by design, can flout them, you face difficult decisions.)

Iterating

Clubhouse, the audio-only social app, has added text-based chatting. A not-infrequent pattern is that a new service offers a stripped down, minimalist, focused competitor to broader options, and then, piece by piece, reassembles the featureset of what it used to compete against. This looks like a purely hype-driven process, but actually makes some sense: every mode of interaction has a different kind of virality, and in the case of live audio there's some powerful fear of missing out: if you don't tune in, you missed your chance! But users have many different interaction preferences, and while acquiring them can require focus, retaining them means giving them lots of options. Microblogging platforms went through a similar process years ago, where they started out being simple and slowly recreated features that Wordpress and the like had had for years. The minimalist approach got them users, but maintaining a network effect requires a different set of strategies than building one.

Bad Funds, Conflicts, and Bias

Morningstar has a look at the collapse of the Infinity Q funds, which produced steady and uncorrelated returns until they a) blew up, and b) ended up being worth far less than their carrying value had been (one fund was liquidated for 25% less than its stated value). The whole point of trading derivatives is that there's room to debate exactly what a financial product is worth. Even something simple and standardized like a call option is open to plenty of discussion (the shape of the distribution for Activision calls, which are a bet on the consummation of a merger at a fixed price, is very different from the distribution that applies to a biotech company in the middle of an important clinical trial). Managing this is tricky, because fund managers have a natural and healthy incentive to believe that they're correct about their valuations, and over time valuations can drift from slightly over-optimistic to outright fraudulent. Which raises the question of what kind of incentive structure avoids this. Big banks have taken their share of derivatives losses over time, but they seem to have the right setup: the bank rents its balance sheet to smart traders, and then has to invest considerable resources and expertise in continuously auditing what those traders are doing to make sure the risks they're taking are fairly compensated by the rewards. When the structure is flatter, and the people risking capital are outside investors with less expertise and visibility, disasters are more likely.

Diff Jobs

- A startup making it easier to share databases is looking for a senior frontend engineer who has data experience. (worldwide, remote)

- A company allowing retail investors to create systematic strategies is looking for an engineering manager. (US, remote).

- A startup creating a tool for SMBs to handle vendor management is looking for backend engineers. (US, remote)

- A startup creating an emerging market bank for SMBs is looking for a Head of Product. (London)

- There are companies across crypto, fintech and edtech looking for data scientists.

Kids are great for economic growth because they drive a lot of incremental consumption—bigger houses, bigger cars, lots of childcare and education-related spending, not to mention clothes and food. And then they grow up to be adults, who are hopefully productive taxpayers. This aligns well with a financial lifecycle where their parents are net borrowers early on, and then pay down debt and accumulate savings in their peak earning years, with those savings partly flowing back to fund the borrowing of the next generation of parents. Retired people also produce consumption, but of a less productivity-enhancing and more deflationary kind: their marginal consumption goes down in most categories but rises steeply for healthcare, and since healthcare is a labor-intensive job where it's hard to find incremental efficiencies, but older people are overrepresented in the electorate, this tends to mean that economic activity shifts towards healthcare without seeing many increases in productivity. All dependency ratio changes are not created equal: the childbirth-driven rise in the ratio from the 1950s onward was associated with faster growth, while the aging-driven one we're in now has mostly slowed the economy down.

Some countries go to great efforts to affect how many kids families have, with mixed success. We'll know Hungary is serious about its many efforts to increase childbirth if the best-paid engineers and product managers in the country are all working for a state-funded online dating app. Countries willingly nationalize energy companies and other strategic businesses even though it's possible to import substitutes, but it's hard to import an online dating ecosystem with the right incentives. ↩

On the "who pays for what" side, Bumble paywalls certain search filters, like height, education level, and lifestyle choices. You can be choosy, but only if you choose to pay. ↩

The company previously tracked revenue per subscriber, but they've learned many price-discrimination tricks; some people won't commit to a monthly subscription but will make lots of in-app purchases, so their new metric blends both. (And what dating app company would refuse to understand the needs of a customer who persistently can't commit?) ↩

Full disclosure: I met my wife on OKCupid, back in 2013 when it was good. We are direct contributors to the churn problem: it is deeply unfair but true that if you hate online dating you can blame happily married couples. ↩