Illumina: "View Source" for Life

Here's a quick science fiction story: a five-year-old boy is admitted to a neonatal intensive care unit, suffering from symptoms of infantile eosinophilia, a sometimes deadly disease in which the body produces too many of a particular kind of white blood cell. There are a few dozen potential causes, ranging from asthma to roundworms to leukemia. His genome is promptly sequenced, and a day and a half later, the cause has been identified, treatment has begun, and, a few hours later, the symptoms are receding.

This is a bold vision of how humans might conquer disease in the future; it's also nonfiction. This story was related at an investment conference a few weeks ago by the CEO of Illumina, the $68bn market cap leader in genome sequencing. Illumina is at two different inflection points. First, the combination of lower-cost sequencing and the Covid-19 pandemic imply a much bigger role for sequencing in the future. And second, while the company has an incredibly impressive long-term record, recent performance has slowed and competitors are gearing up to offer cheaper, faster products.

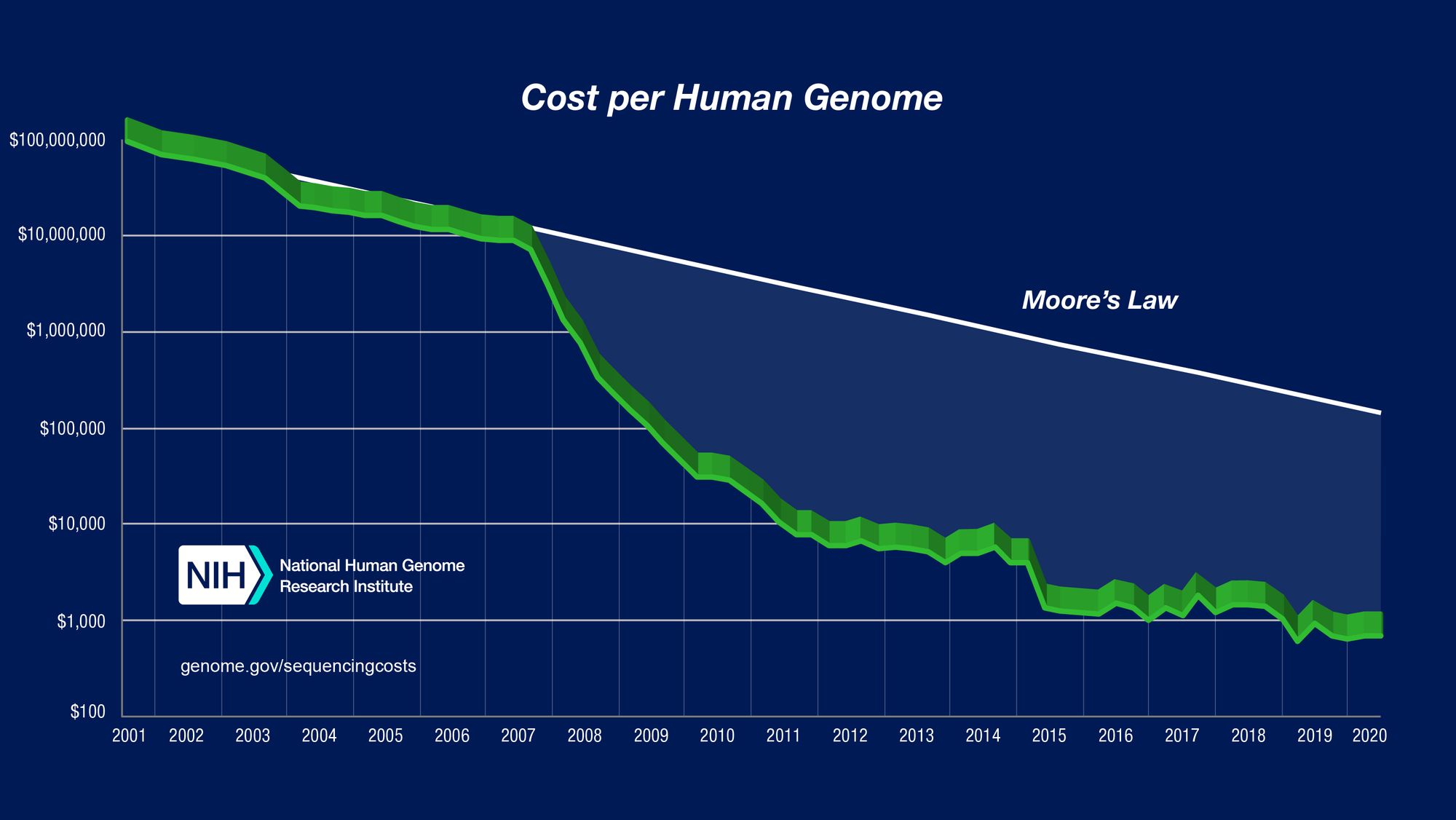

This is an important trend to understand. The plunge in genome sequencing costs in the last twenty years makes Moore's Law look fairly sedate. A world population that's getting older and richer will make cancer treatment a more significant chunk of healthcare, and cancer—a self-propagating bug in the genetic code—is exactly the kind of disease that cheap genome sequencing can have a big impact on.

DNA is the world's most widely-deployed programming language; each of your cells has up to 10 million compilers. The code varies from highly redundant to weirdly reliant on strange hardware hacks, and nothing is documented. Anyone who has compared modern languages to, say, COBOL or MUMPS, will not be surprised to know that this strange, hard-to-read language full of unpredictable behaviors and poorly-understood quirks has been in use for over three billion years. Actually reading and manipulating the genome is the real-world equivalent of buffer overflow glitches in video games like this one. The source code of life can be viewed while the process is running, which is extraordinary.

Reading DNA is nontrivial. In diagrams, strands of DNA are nicely color-coded and usually displayed on a dark background, but in real life it's a tangled blob. Two feet long, 1/40,000th of the width of a human hair; it's a complicated molecule to work with. (To put this in more tangible terms, a DNA molecule the width of a standard garden hose would be 9,000 miles long.) There have been a few quite clever efforts to make cells more readable. Pyrosequencing, for example, illuminates nucleotides using the same enzyme fireflies use to light up, a very biopunk approach.

{kind=link}

Illumina's method is to essentially slice strands of DNA into short segments, attach known segments of DNA to either end of them, generate a bunch of copies through polymerase chain reaction, apply reagents that cause individual nucleotides to light up differently based on their contents, and then use bioinformatics software to stitch the sub-sequences back together into one long sequence by looking for overlapping patterns. Reading small segments with overlapping information lends itself to parallelization: the 3.2 billion base pairs in the genome are cut into segments as short as a few dozen base pairs, then read at the same time. This allows Illumina's devices to ingest 1 billion base pairs per day; an entire genome can be read for $600.

That $600 quote should be quite striking. The Human Genome Project spent a decade and $3bn to get to a "rough draft" sequencing. In 2007, sequencing 90% of the genome cost about $100,000. In 2010, the cost hit $10,000. That cost curve sounds like Moore's Law, but was actually quite a bit faster from 2007 to 2015.

A $100 million genome is an expensive proof-of-concept, or a ludicrous Veblen good for the plutocrat who has it all. A million-dollar genome may be worth doing for research purposes. A $50,000 genome gets to the point that everyday rich people who care about their health will give it a shot. But when the price gets down to the $1k range, or below, the possibilities get very exciting:

It can help with drug trials, by identifying genetic differences that affect how people respond to drugs. A drug that works 10% of the time is very different from a drug that works 100% of the time for 10% of the population, especially if membership in that 10% can be tested in advance. It can also help identify potential drug mechanisms, something that's already happening.

It can help the agricultural sector understand how genetic variations affect crop yields—very useful for GMOs, but good to know regardless.

It allows affordable prenatal testing, which can screen for genetic disorders.

It allows for more precise embryo selection ($, Economist), both by knowing exactly what's in the embryo and having a larger sample size for what those genes might mean.1

It can assist in detecting and treating cancer. "Cancer" is a broad category because it's a mutation, and there's significant variance in how treatable cancers are. Sequencing the cancer genome is a good way to identify treatments that typically work for other cancers and can be applied to this one. (This has been happening since a decade ago.)

It's very helpful for understanding and curing novel infections. The book The $1,000 Genome, published in 2010, quotes the CEO of 454 genetics: "There's really an amazing possibility now of preventing another HIV epidemic, another SARS... Had we been around in the early '80s, when HIV started popping up, my personal conviction is that the epidemic wouldn't have existed." Roughly true! Patient zero's Covid symptoms started on December 1st, 2019, the sequence of the virus was posted online on January 11th, and two days later Moderna had designed mRNA-1273, a substance that many of the people reading this have had jabbed into their arms recently. That's 43 days from the first known infection to the cure; the equivalent for HIV would have been a working vaccine in the 1960s.

All of this is naturally very beneficial to Illumina. More users are nice, and more usage is even better. While Illumina is nominally in the business of building sequencing machines, 71% of their revenue last year came from the reagents consumed by each test. As many, many other companies have discovered, it's far better, from a planning perspective and a market value perspective, to sell something that leads to continuous spending rather than lumpy one-off spending. If it works for crafting tools ($) and car washes ($), it can work for DNA sequencers.

The trouble Illumina is running into now is that the wonderful better-than-Moore's-law experience curve for genetic sequencing has also had a faster-than-Moore's-Law slowdown. 2007 and 2008 were incredible years, with the cost of sequencing dropping by 84% and then 90%. But since then, the rate has declined; over the last five years, the compounded average is -24%, which is actually slower than the five-year pace as of 2007.

The other risk they run is exemplified by the Covid example above. Careful students of history will note that the pandemic did not end in January of 2020 when a vaccine was developed. While the trials and approval process were fast as far as such things go, only making time for essentials like four-day weekends (during which 44,050 people died of Covid). But most approval processes take longer. As genomics works its way into treatment rather than pure research, the risk of regulation rises—and that risk is not just from restrictions on what Illumina's users can do, but on how long it takes for them to get permission. Moore's Law would have had a very different impact if every new PC went through a multiyear approval process before getting sold. (The fate of the Xerox Star—which did go through a lengthy approval process of sorts, driven by Xerox's internal politics—is an illustrative example.)

Meanwhile, Illumina has competitors to worry about, not to mention a whole different set of regulators. They tried to acquire Pacific Biosciences for $1.2bn, but got blocked by the FTC. (This would have been a good move; two years later, PacBio is worth $6bn, and recently raised $900m in convertible financing from Softbank.) Oxford Nanopore is preparing to go public, and is also planning to use multiple classes of stock specifically to prevent a takeover ($, FT) (it's worth noting that Illumina's 2007 acquisition of the British company Solexa put them on their present course). Oxford Nanopore's technology can be cheaper—sequencing is more expensive, but the equipment is orders of magnitude less pricey, although this comes with an accuracy tradeoff. Illumina spun out its blood-based cancer screening company, GRAIL, in 2016 and tried to buy it back last year, but the deal may be blocked.

So the company is stuck in an awkward position, where it dominates a market but can't easily expand through acquisitions, and faces direct competition. For a long period, Illumina acted as a protagonist in genome sequencing (and its stock is priced accordingly, at 16x next year's sales and 55x next year's EBITDA), but it's increasingly a bystander, facing regulatory risk both for strategic decisions and product decisions. Illumina might be able to keep pushing costs lower for a long time—when I talked to people in the industry, the most common verdict was that they're resting on their laurels—but that decision only works if new uses for genomics are a) invented, and b) allowed. As the cost declines, the revenue-maximizing uses of genomics have to be more widespread; there's a price point at which it saves health insurance companies money to use annual blood screening to test for cancer, for example, and a higher price point at which it makes sense to sequence every cancer that develops in order to treat it better. Extrapolate ten or twenty years and you can get to lower costs and more extreme bull cases: gut microbiome health is important, so why not test people more or less continuously (weekly? Daily? Hourly?) to see how their gut health is doing? It's conceivable that genomics could be the part of the healthcare system that people interact with more frequently than any other, and that's a very good future for Illumina (or its competitors!), even at low price points. The Jevons paradox served industries like semiconductors, oil, and cell phones well, but it requires a leap of faith: cutting prices enables more usage, but that's only meaningful if there are novel (and legal) uses.

A Word From Our Sponsors

Here's a dirty secret: part of equity research consists of being one of the world's best-paid data-entry professionals. It's a pain—and a rite of passage—to build a financial model by painstakingly transcribing information from 10-Qs, 10-Ks, presentations, and transcripts. Or, at least, it was: Daloopa uses machine learning and human validation to automatically parse financial statements and other disclosures, creating a continuously-updated, detailed, and accurate model.

If you've ever fired up Excel at 8pm and realized you'll be doing ctrl-c alt-tab alt-e-es-v until well past midnight, you owe it to yourself to check this out.

Elsewhere

The Balance Sheet-Constrained Bank

A well-run company operates at the limit of various constraints, so company behavior can often be a good indicator of which parts of the economy have slack and which are operating at maximum capacity. In banking right now, there's a crisis of abundance—lots of liquidity, relatively few places to put it. So banks are mostly unconstrained in how much they can lend. This makes it hard to see which parts of the credit market are more or less promising. One bank, though, does have limits: Wells Fargo's balance sheet was capped to punish it for the fake accounts scandal a few years ago.2 As a result, Wells Fargo is eliminating its personal line of credit product, suggesting that customers use credit cards and personal loans instead. Since Wells Fargo pitched these credit lines as a way to consolidate credit card debt, these lines of credit a) appeal to people who have credit card debt outstanding, and b) carry a lower interest rate. So Shifting these customers back to credit cards is a way to get higher returns on some of Wells Fargo's assets, while trimming the total so they can comply with their regulatory limits.

The Global Kuznets Curve in Action

A few weeks ago I wrote about how the inverted-U relationship between GDP per capita and pollution was changing as globalization linked policy and as more pollution concerns focused on greenhouse gas emissions rather than localized problems. A compelling recent example of this is Bangladesh's decision to cancel the construction of ten new coal power plants ($, Nikkei), citing environmental concerns. Coal is hard to dislodge once it's installed, but anyone who builds a new coal power plant today has to consider the liabilities they're accruing over its next few decades of operations.

Net Zero

Amazon advocated higher corporate taxes while lobbying for R&D tax credits. To the extent that the only available positions on taxes are that they should be higher or lower, this is hypocritical—Amazon wants it both ways! On the other hand, it's entirely possible to argue that the tax code ought to be smarter; when I think about ways I'd alter the tax code, I usually assume the goal is to be revenue-neutral but lead to better decisions. If corporate taxes go up, it will make the value of Amazon's R&D-related deductions and tax credits relatively higher—if the ultimate result of that is lower aggregate corporate taxes, that's only possible with an increase in corporate spending on R&D. Amazon can save a lot on taxes if it reinvests all the money it makes in R&D. While that research can cause more economic power to be concentrated in Amazon, which raises its own problems, it also has benefits. Research tends to generate positive externalities, which are hard for the creators to capture; all of the world's trillion-dollar companies exist because of inventions from Bell Labs, but none of them are paying material royalties to AT&T for the privilege.

(Disclosure: I'm long AMZN.)

Real-Time

Payments and savings are on a continuum, but that's only apparent at two extremes. For huge companies, managing cash needs is important because there's enough cash on hand that any slight over- or under-allotment will have a financial impact big enough to justify someone's full-time attention. And for people with low savings, the timing of cash flows matter because they can be one surprise bill or one late paycheck away from insolvency. PYMNTS looks at this dynamic, especially around slow clearing for financial transactions; if you're living paycheck-to-paycheck, the difference between a check clearing on the Friday before a long weekend or the Tuesday after can be very material. One important piece of evidence for this is that half of the customers of check-cashing stores have bank accounts; it's not that they're underbanked so much as misbanked, and slightly faster clearing alleviates this problem. As banks pull back on overdraft fees, the issue may be alleviated; from the perspective of someone living paycheck-to-paycheck, this amounts to lowering the interest rate on a check-cashing alternative. But it's still an illustration of how much financial plumbing matters, in both a micro and macro sense.

Aviation’s Big Two (Plus One)

China's state-backed aircraft manufacturing company, COMAC, has neared approval for its 168-seat C919 plane ($, FT). The passenger plane business has been a hard one to compete in, with smaller players slowly getting absorbed or defeated by Boeing and Airbus. As with other national champions in China, COMAC has the advantage of a large and growing home market. COMAC also gives China's government another degree of freedom in negotiating economic relationships with other countries; since the aircraft industry is rewarded by scale, incorporating plane purchases into trade and loan deals can be cost-effective. It's still not a completely independent industry; as the FT notes, COMAC is still sourcing components from the US, Germany, and France. So, like many other aspects of China's economic growth, it trades off short-term interdependence for long-term independence ($).

This is, for many reasons, a whole lot more controversial than, say, selecting for high-yield, pest-resistant corn. It's also very hard to stop. Parents will go to extreme lengths to get their kids a leg up, both legal and not. Arguably, to many members of the elite, the status conferred by Ivy League degrees is more sacred than the stuff of life itself. Competition between superpowers also makes it hard to restrict; anything that American refuses to permit on ethical grounds is something China is the default winner at, so in these matters both countries will end up at rough parity where bioethics is concerned. ↩

This incident often gets misportrayed. It was not a straightforward story about Wells Fargo signing customers up for expensive services they didn't want; it was a story about the company's employees signing customers up for mostly-free services they didn't want. Wells Fargo's management is culpable for 1) setting a poor metric for measuring employee performance, and 2) having done that, failing to audit employees to make sure they weren't following perverse incentives. ↩