Who Reads The Diff? (+ Reader Survey)

Not gonna lie, the subject matter of The Diff is eclectic. I’ve written about SaaS economics, market manipulation, Numismatics, online recipe SEO, and a DTC IPO, and that’s just since January.

Who reads this stuff?

It’s an amorphous group: startup founders, college students, college professors, venture capitalists, hedge fund analysts, engineers, executives, “independent researchers” (i.e. people who are willing to live on ramen if it means they can pursue the intellectual interests they want), “independent researchers” (people who bought Bitcoin at $1 or something and will never have to work again), and a long tail of other people. Also, 1.25% of the Forbes 400.

What readers have in common: caring about the future, and wanting to act accordingly.

It would be great if you’d fill out this quick reader survey.

The Residential Real Estate Market is Basically Fine, For a Bad Reason

The financial crisis left some battle scars, and one of them is the reflexive association between “housing” and “disaster.” I’m on the record arguing that housing is a bad investment, and that the way Americans finance housing is deeply harmful—but that’s because I view housing as a bad investment at a personal level. It’s a way to double-down on local labor markets, which is not a bet most people should make.

At an aggregate level, though, housing prices are not so bad.

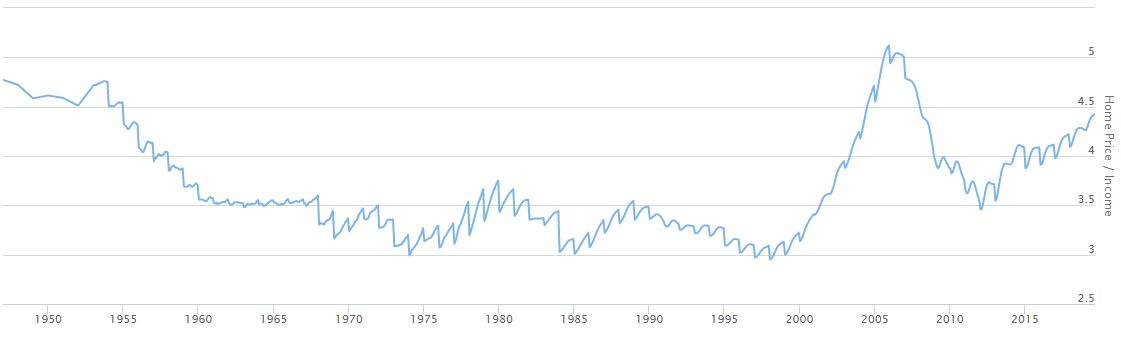

If you look at overall housing prices to incomes, you might get nervous:

But it’s worth doing a deeper dive into the data. I looked at the Case-Shiller city-level indices, and the US Census’ county-level average income data. (Both conveniently available on FRED.)

A house represents many bets, but the most meaningful of these is that it’s a bet on local wages. Since wage-earners are the marginal bidders for most homes, cash comp sets prices. Over the last twenty years, changes in median household income explain roughly 70% of the change in city-level home prices. Median wages in Cleveland rose 1.3% annualized in the last twenty years, and housing prices rose at the same pace. Median wages in San Francisco rose 4.3% over that period, and housing prices rose 6.2% annualized over the same timeframe.

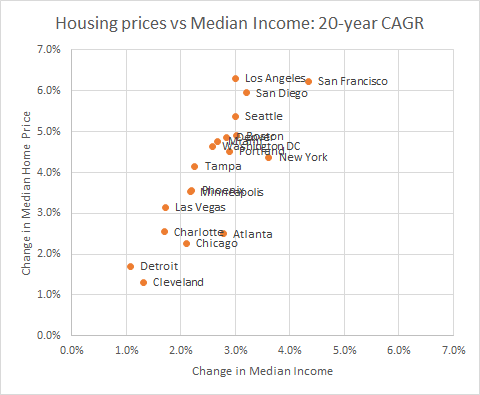

Here’s the full data:

Excel wanted me to shrink the range of the X axis, because there aren’t any major cities with median wage growth above 5%, while four different cities had housing price growth at those levels.

The best way to make the comparison is to use yet another dataset to get median home prices in each city, which I can compare to the nationwide average. SF houses are 2.7x the national average in this model, while Cleveland is 0.42x. We can use these stats, along with average income, to compute the number we really care about: if you earn the median household income and live in the median city, and you move somewhere else, how long is your payback period?

The answer varies a bit, likely driven by gaps between where people live and where they work, or slightly different definitions of the relevant geographic areas. But they do give you a broad sense for a worker’s “P/E” ratio for buying into living and working in a particular city. Housing prices in the greater New York area are $94k above the national average, while Manhattan wages are $21k above average, so New York has a low P/E if you’re willing to commute. Boston is expensive, with a $5.5k wage premium and a $97k housing premium. SF’s P/E is about 12 by this measure: for a $550k housing price premium, you get a $47k wage premium.

The “median worker” is, of course, fictional. But in some job categories, it’s a useful fiction. If you write code, you can write code from anywhere. It’s not a coincidence that the cities in the upper-right corner of the graph are all tech meccas, while the ones on the bottom left are in the rust-belt. Human capital is mobile; factories are not.

So you can look at a rising price-to-income ratio as a rational calculation on the part of some workers and homeowners: they pay a larger percentage of their income to live in a particular place, but in absolute dollar terms they can end up better-off. If you go from earning $80k in Dallas and spending 25% of it on rent to earning $160k in SF and spending half on rent, your housing-to-income ratio is trashed but your post-rent income rose by a third.

It points to two separate problems, both involving economic, rather than literal, rents.

Rising Housing-to-Income Ratios as the Double-Rents Problem

Economic rents have two connotations: the neutral-to-questionable one is that they’re profits above the cost of capital, and the negative one is that they’re profits extracted from more legitimate activity. Stephen King earns rents by having a monopoly on Stephen King novels. Isabel dos Santos earns economic rents by doing business with a state oil company owned by her dad.

Both senses of rent matter here. Positive wage pressure is from the neutral sort of rents extracted by Microsoft, Apple, Google, Amazon, etc.: monopolies on things people like. But those rents shouldn’t necessarily translate into higher real estate prices—Amazon employees don’t have to pay a premium to buy a car or a nice dinner, for example.

The bad sort of rent-seeking is engaged in by landlords, with the tacit cooperation of environmentalists and general NIMBYs. They exercise a de facto veto on new housing development. You can see ridiculous stories about the tactics these groups use, from fictional secret tunnels of great historical importance to actual laundromats of fictional historical importance to shadows, shadows, everywhere.

This has led to a drop in the elasticity of housing supply throughout the country. And, if I remember my Econ 101, inelastic supply leads to prices that are responsive to demand. Higher housing costs benefit companies that can pay high cash comp over companies that pay more in options and cachet. They’re a relative subsidy for today’s tech monopolists, at the expense of the possible monopolists of tomorrow.

The real danger of rising price-to-income ratios for housing is not that housing is getting less affordable—it’s that housing is perfectly affordable, so long as the profits from building new tech companies accrue to lucky landlords rather than founders, employees, and investors.

Elsewhere

The Bay’s tightly-restricted real estate market has claimed many victims. The latest: an anarchist hackerspace:

What makes SF what it is? Anarchists launching woodworking projects and crazy 3D printing schemes, or building inspectors and landlords?

An interesting pair of funding announcements: $6.5m for a company that makes static Wordpress templates, and $15m for a company that makes it easier to design Wordpress sites. Wordpress is one of those platforms that quietly became ubiquitous: it’s common enough that Wordpress services can use Google Maps spam to market themselves. When a pure software product starts to show up in the real world, it’s a big deal.

The trouble with building on one platform is that it’s market research for the company that owns that platform. Most great platforms start out open, identify the value being created (and the negative externalities being imposed) and slowly close off. This is not because they’re cynical; it’s just a fact of life that once you interact with hundreds of millions of people, you’re forced to become a politician. But it should worry investors in these startups, since the endgame is either to get bought or to get squeezed.

Platforms grow because they’re useful, and when they’re really useful, people start to depend on them. So every good tech company is born as something cool and evolves, if it’s lucky, into a high-margin utility, with the usual public-interest provisos. This puts tech companies in a bind: they can be “fair” in the sense of equal treatment, or “fair” in the sense of equal outcomes, but they can’t do both unless they exist in a world that’s perfectly fair. Pete Buttigieg and Andrew Yang had better email marketing teams than other candidates. Beto really didn’t. (This is basically in tune with the vibe of both campaigns: Pete would put someone generically competent in charge, and Yang would hire someone who liked optimizing.)

Hart-Scott-Rodino triggers FTC reviews when an acquisition passes a certain size threshold. “Size” is determined by assets, because HSR was signed in 1976 when most acquisitions were still companies-with-stuff buying other companies for their stuff. Now, it’s basically arbitrary. But when a company gets sold and it’s close to the threshold, antitrust review is an annoying practice.

So:

Something unusual was underway in early 2010 at Invite Media, a Philadelphia-based advertising technology startup. Under normal circumstances, it collected money from marketers and used it to buy digital ads. But over two days that spring it suddenly began paying for a wave of ads without waiting for checks to come in, using its own money instead. The company also paid off all its outstanding bills regardless of their due dates, sending its bank account balances plunging.

It would normally be irrational for a company to burn cash unnecessarily, but in this case burning cash was the whole point. Invite’s co-founders were finalizing a deal to sell the company to Google, and reducing Invite’s assets was a key part of their preparation. By drawing down its bank account, Invite could reduce its total assets to a low enough level that the companies could avoid submitting their deal for review to the Federal Trade Commission, according to three people familiar with its finances.

The immovable object of regulatory attention meets the irresistible force of financial engineering!

Games like this have a positive expected value with negative skew: normally, they mean less paperwork and fewer delays. Occasionally—i.e. right now—they mean retroactive scrutiny. And now, not only does the FTC want to look at the acquisition, but they want to look at it as an acquisition that involved something worth hiding.