In this issue:

- What Can You Learn from a Deterministically Chaotic Market Simulation?—It's hard to build market simulations, because you're only simulating the market well when your simulation occasionally produces results as weird as the crash of 1987 or the meme stock boom. And these simulations need to deal with many interactions at once, so when they don't work, it's hard to tell how broken they actually are. But when the cost of writing and debugging code drops by a few orders of magnitude, it's finally possible.

- Prediction Markets—One regulatory advantage public markets have is that we have a discrete way to decide that some piece of information is public or not.

- Exotics—You can manufacture a derivatives bet that markets will keep grinding up until they suddenly collapse. But that's close enough to the default expectation that it's going to be expensive.

- Binning—Having a very tightly-managed supply chain means that loosening up a bit can pay off.

- Unpopular AI—If you use wide age buckets, AI is more popular with young people than old people and with educated rather than uneducated people. But choose a sufficiently narrow slice—people who flip education categories from "Some College" to "College" in the next couple hours—and they'll really hate AI.

- The Rebalancing Trade—BlackRock may bet on SpaceX, but it's also hedging a bet that its passive vehicles have to make.

Talk to this post with Read.Haus.

What Can You Learn from a Deterministically Chaotic Market Simulation?

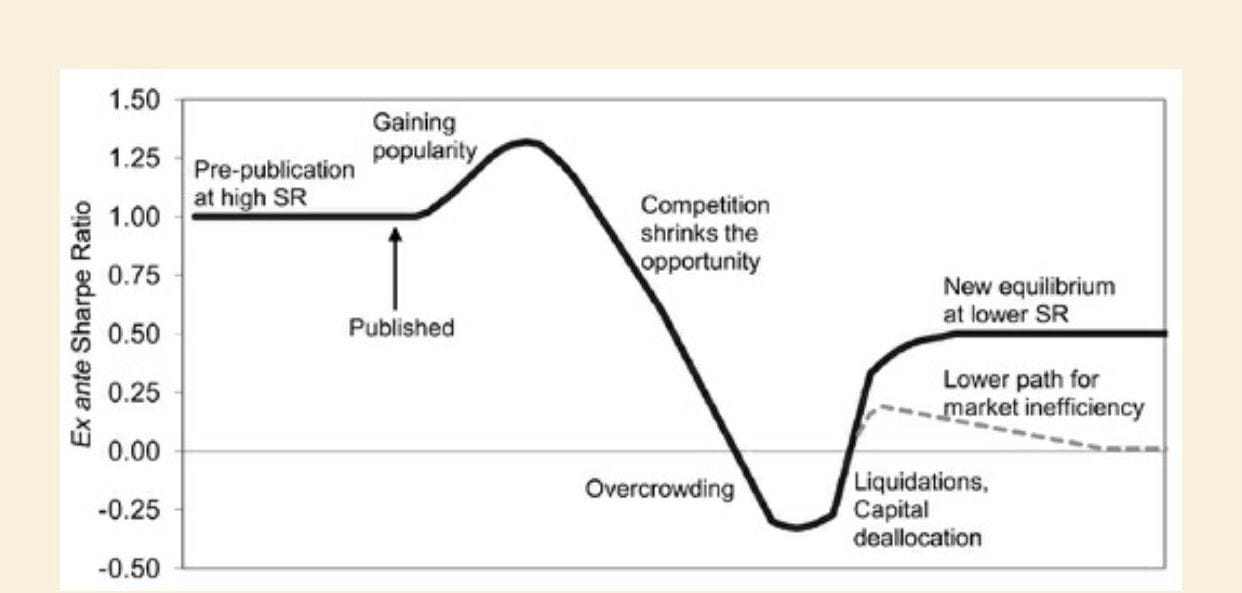

The most beautiful chart in finance is the stylized one from Expected Returns showing the life cycle of a trading strategy: there's alpha for a while, it gets devoured, and often, there's a point where the strategy overshoots and people actually lose money running it. So:

It would be nice to get real-world confirmation here, but many real-world strategies are noisy. If you're paying for something like momentum, or value, or risk arbitrage, or whatever factor you care about, you are presumably paying someone to do something other than mechanically follow a simple strategy, which means that crowding is a kind of amorphous concept. Someone running a principal component analysis on every quant portfolio in the summer of 2007 would have found Platonic forms of the various bets they were making—momentum persists, value mean-reverts, companies with high and stable margins outperform, high-yielding currencies overcompensate you for their risk—but it won't necessarily show up in any publicly-available backtest.

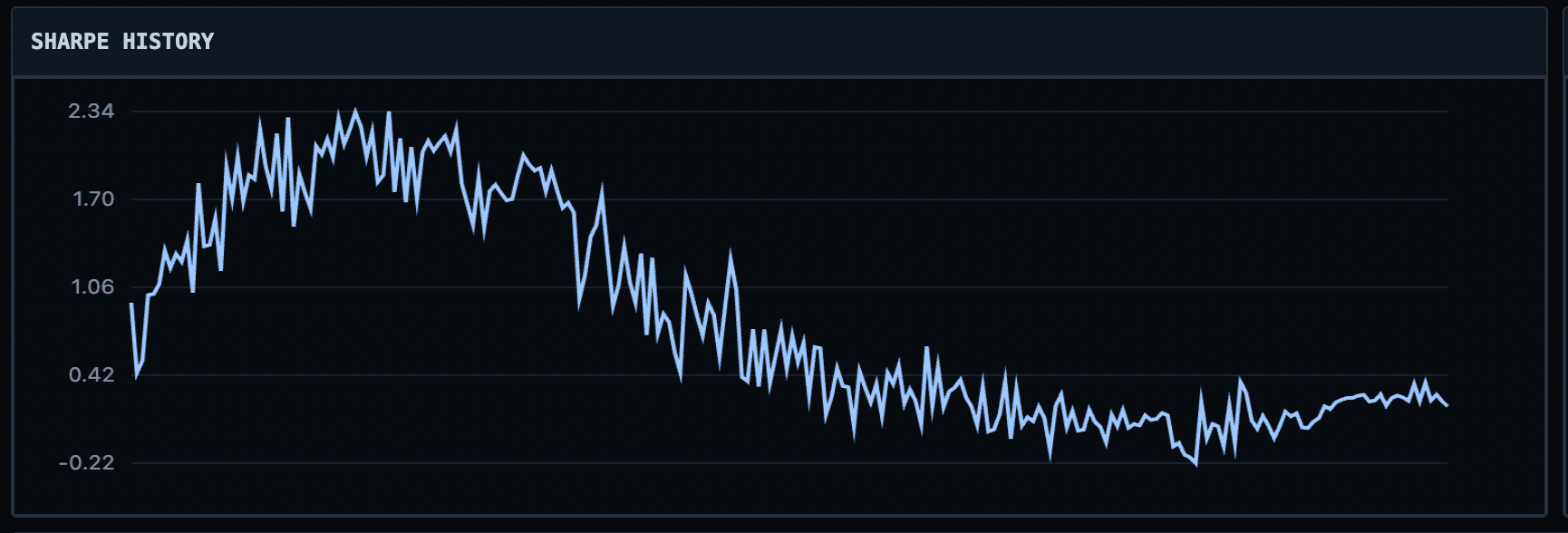

But you could take a look at this:

The magnitudes aren't quite the same, but then again the first one was a stylized chart of a hypothetical way things could go. This one's a real factor—going long companies in proportion to how much of their market cap they're buying back, and shorting companies in proportion to their annual dilution. It goes through cycles, because you can have too much money outsourcing its thinking to managers who are subject to the same human biases as the rest of us. In this case, you can define the exact parameters of the factor bet, and measure the exact contributions, because the whole thing actually takes place in an agent-based simulation full of different trader agents executing slightly randomized variants of different strategies. And yet, it's able to pick up on something spotted by practitioners in the real-world domain that simulation is a model of.

A realistic market simulation is hard, because "realism" needs four forces to be roughly balanced:

- Noise traders buy and sell stuff at random, or at least can be modeled that way. (In practice, it's probably better to say that noise traders have reasons to make trades and that these reasons roughly cancel out.)

- A market is pretty boring without traders who have some concept of fundamentals.

- You also need companies to do corporate finance: issuing stock when their share price is high, buying it back when it’s low, paying a dividend, etc. All of this anchors prices and means that agents in that market who make sensible decisions will be a bigger factor in the overall market over time.

- And you need market-makers, who just quote a price at which they'd buy and sell. (It simplifies the model a lot if you arbitrarily decide that limit orders are for market-makers and market orders are for everyone else.)

This means that this is the kind of software product that's hard to build in small increments. There are parts you can build and test, but what you're really testing is an entire system that can get to some kind of reasonable equilibrium, where prices wiggle around in what might be a random walk. And it's hard to do that while optimizing four distinct things at once. Even more annoyingly, one of the marks of realism in an equity market simulation is that it can reproduce events like the largest companies in the world's most important equity market losing 20% of their value in one day for no particular reason, or shares of a large automaker rising fivefold in a few months during a financial crisis, or shares of a negative-growth video game retailer rising in value by two orders of magnitude in a few months.

But if you can get it working—if you can get a model to the point where different people will figure out different fundamentals at different times, meaning that momentum can actually work, and that this combination means that there's a back-and-forth for market-makers where they spend some time profiting from uninformed customers and the rest of the time accidentally providing liquidity to very sophisticated ones, then you can actually get to an equilibrium where different approaches go through booms and busts, and these affect the availability of capital to different companies.[1] Specifically, you can build a system where both value and momentum work, as entirely emergent properties of traders with randomized but understandable preferences interact with companies that are simulated under the same criteria.

One of the great paradoxes of systematic investing is that value and momentum sound like opposites, but doing either one of them makes money over time and doing both at once tends to make a bit more. But that shouldn't be the case at all! Momentum involves buying whatever has been going up a lot already, and value involves buying whatever is statistically cheap, ideally relative to some stable measure like book value rather than something more ephemeral like earnings or dividends. So, from a fundamental perspective, they're opposites: one's betting on mean-reversion, arguing that book value is a better proxy for intrinsic value than market price. And the other feels more nihilistic about valuation: the right price is whatever it'll trade at in a month if this month is exactly like last month.

But they're both also bets on inferred private knowledge: someone who is stratifying their investable universe on the basis of price to book value is implicitly saying that they trust any accountant more than they trust every market participant, weighted by how much they want to trade. Meanwhile, momentum says: I trust whichever market participant is in such a hurry to bet on this company that they're willing to move the price.

Both can obviously go wrong, but on average they've both historically turned out to be right. Accountants are giving you a way to buy assets for below replacement cost, which often means buying assets based on an earnings multiple and then benefiting when that earnings multiple expands, but not by enough to attract new competitors. Momentum is giving you an indirect read on the views of people who have high conviction and haven't gone broke yet.

In both cases, they're prone to following a cycle where capital inflows push prices in the direction that recently-successful strategies expect, which, of course, pushes those prices past where they ought to be. But that process ultimately gets anchored to real-world variables. There is some difference in how fast different people learn new important facts about the world and figure out their implications, and when that gap is big, momentum performs better. At the same time, insiders know more than outsiders, and if a CEO thought some piece of equipment was worth buying at some price, and an accountant agreed on how long its useful life was, then there's a point at which betting that they're generally right is higher-return than betting that they're overconfident.

An agent-based model isn't proof that this is a natural emergent property of markets where participants look at things differently and have different access to information. But it's pretty compelling if simulations can produce results like these.[2] But one of the strengths of agent-based modeling is that if you can describe certain behaviors as inputs, and they feel recognizable, and then you can describe the outputs of the model and they feel recognizable, it's probably subjecting things to a process that's similar to whatever real-world phenomenon it's trying to replicate. The other takeaway from all this is: the longer you've wanted to attempt some technical project, the more precise your prompts are likely to be, and the bigger a force-multiplier LLMs will be. The cumulative stock of over-ambitious technical projects pursued by not-technical-enough people is yet another category subject to the sonic boom of LLMs.

I'd messed around with this off and on since 2019, generally getting to the point that I had a hard-to-debug mess and then starting over. 24 hours of intermittent Codex effort got to a backend that can simulate about 4,000 trades per second, following a couple dozen discrete strategies, and can also display it in a nice browser-based UI with decent-looking charts. ↩︎

It didn't just recreate phenomena like crowding and blowups. In one instance, I got a compounder! There was a company whose steady-state ROE was higher than average, and that also had a preference for returning little capital, so, under the assumptions of the model, it could grow indefinitely, and various implementations of momentum figured out that it could keep going up, too. ↩︎

You're on the free list for The Diff. Last week, paying subscribers read a profile of Lincoln Internatinal, a low-profile but very profitable investment bank that's finally going public ($), thoughts on the unusually leaky SpaceX IPO ($), and how AI will produce a sonic book of transparency ($). Upgrade today for full access.

Diff Jobs

Companies in the Diff network are actively looking for talent. See a sampling of current open roles below:

- Ex-Anduril, Ex-Abnormal Security, Ex-Bridgewater, fast growing startup bringing agentic cybersecurity to 99% of businesses via MSPs is looking for platform and machine learning engineers. Startup experience preferred; what matters most is that you've grown in scope and handled ambiguity over the last few years. (SF)

- Series A startup building multi-agent simulations to predict the behavior of hard to sample human populations is looking for a founding recruiter who’s able to attract and close the best research and engineering talent in the world. Experience building high-quality teams as a former founder, VC, or operator a plus. No formal experience in a “recruiting” function required. If you have experience communicating and persuading smart, disagreeable counterparties of your vision, this is for you. (NYC)

- AI Transformation firm with an ambition to build an economic world model to run swathes of the private, unstructured economy is looking for FDEs, Platform Engineers, and business generalists who understand how to solve problems.

- Well-funded, frontier AI neolab working on video pretraining and computer action models as the path to general intelligence is looking for researchers who are excited about creating machines that learn from experience, not text. Ideally you have zero-to-one pre-training experience and/or are a high-slope generalist who’s frustrated that the big labs aren't doing this. (SF)

- Lightspeed-backed team building the engineering services firm of the future is looking for founding members of technical staff excited about working alongside civil engineers to translate their domain expertise into the operating system that powers the next era of great American infrastructure. If you’re an engineer with strong product intuition, who's energized by access to users, and excited by the prospect of transforming how we design and construct our built world with frontier AI, this is for you. (NYC, SF or Remote)

Even if you don't see an exact match for your skills and interests right now, we're happy to talk early so we can let you know if a good opportunity comes up.

If you’re at a company that's looking for talent, we should talk! Diff Jobs works with companies across fintech, hard tech, consumer software, enterprise software, and other areas—any company where finding unusually effective people is a top priority.

And: we're now actively deploying capital into early-stage companies through Anomaly. Our focus is on defense, logistics, robotics, and energy. If you'd like to chat, please reach out.

Elsewhere

Prediction Markets

The US government has requested data from Kalshi and Polymarket about suspiciously well-timed trades ($, WSJ). It's actually very hard to decide the precise line between good analysis and nonpublic information. Ironically, the financial services sector, which has dealt with its own insider trading scandals over the years, has a pretty decent answer: companies are required to file a form 8-K with the SEC whenever they make some material update, so in a sense everything that's omitted from an 8-K (or other company filing) is immaterial if communicated to someone else. That's not the kind of standard any compliance department wants people to follow, but at least roughly describes the status quo. For trading on military operations, senate procedural arcana, etc, there isn't as good an oracle for what's already public and what isn't, so the prediction markets will have to come up with their own standards and defend them from governments who want stricter rules and from users who want fewer false positives.

Exotics

The business of non-standard options is basically a continued financial tug-of-war between people whose unique information tells them about an opportunity to make some kind of nonstandard bet, and counterparties who come up with a way to hedge such bets. Given that any given hedge fund is only intermittently in the business of trading exotic derivatives, but liquidity-providers are always in that business, it's pretty straightforward to see where the edge is. Still, it's notable that many investors are accumulating lookback put options, whose strike price resets higher if prices rise after they're bought. The bet they're making is that prices rise for a while longer and then suddenly plunge, but that describes the vast majority of market regimes: most of the last century has been a slow grind up, a few exciting weeks and months have included big plunges, and that's most of market history. One thing all this says is that capital allocators think that the AI boom is predicated on capital inflows rather than operating profits, so there isn't a coherent world where new funding slows down and it doesn't cause some parts of the AI supply chain to suddenly lose much of their value. And this in turn means that the pain trade is that AI follows the trend of the last few months, of being a mildly pleasant surprise that's either at or above the usual trendlines.

Binning

A weird feature of the computer chip business is that it involves large-scale manipulation of matter at close to the atomic level, which entails unbelievably precise machinery. And, also, it doesn't always work, and some chips end up with cores that don't work. Fortunately, those chips can be repurposed for use in slightly lower-end devices especially later releases ($, WSJ). It's a nice demonstration of the many advantages of scale: Apple sells enough devices at enough price points to predict demand for a new budget option, and its marginal cost for some of the priciest components of that device is lower if it can reuse chips that weren't quite good enough for the top-of-the-line phone. This also illustrates that Apple's obsession with managing its working capital well doesn't preclude it from occasionally sinking cash into something that will take a while to return: doing this means holding more inventory (either directly, or forcing suppliers to do it and pass through the cost). Being generally obsessed with dependable manufacturing and an inventory-light model sometimes means having unique exposure to an opportunity to relax that constraint.

Unpopular AI

If you look at polling data, you'll see that the biggest skeptics of AI tend to be older. That's a pretty consistent historical pattern with new technologies. But the single demographic for whom AI is most salient has to be people who made the decision to get (and pay for) a degree four years ago, and are now graduating into a job market where that degree signals that their capabilities are pretty similar to what cheap models can do elsewhere. So, of course, a tech executive who talks about AI in front of an audience selected to face the most economic pressure from AI is going to get some boos. There's a nice symmetry here with stories about ubiquitous academic cheating with AI. If there's a credential that you can get entirely by using some subscription product, the cost of that subscription is an upper bound on the market value of the credential. This definitely doesn't mean that these jobs have disappeared, it just means that the default credentialing institutions move more slowly than the labor markets they feed: if colleges are giving you what amount to prompts, and if ChatGPT can produce an A+-worthy response to those prompts, you have to figure out how to come up with novel, economically-valuable prompts on your own because you know there are tools that can easily fill in the answer.

The Rebalancing Trade

BlackRock is considering a $5-10bn investment in the SpaceX IPO through its active funds ($, The Information). One reading is that this is an investment in SpaceX, a vote of confidence in Elon Musk, etc. But there's a more bland explanation: BlackRock manages about $9.5tr of passive index funds, which will buy a chunk of SpaceX when it's added to the relevant indices—which won't be instantaneous. This will be a massive company-specific index-rebalancing, though it's probably in the $1-3bn range depending on how big the IPO ends up being and where it trades after. So at least some of this trade is rebalancing, and some of the rest is giving active strategies exposure to something that will end up being part of their benchmark after the IPO. If nothing else, it's an illustration that IPO dynamics around this year's megadeals will be weirder than we're used to.